Ahead of the ten year anniversary of the EU referendum on 23 June, UK in a Changing Europe experts have written a short series of blogs reflecting on some of the issues at the heart of Brexit then and now. Here, Jonathan Portes looks at the economic impact of Brexit.

Brexit was always an economic trade-off. It was a decision to move away from deep integration with the EU in exchange for greater domestic control over migration, regulation and trade policy. The question was never whether this would involve costs. It was how large those costs would be, how quickly they would appear, and whether the gains from autonomy would offset them.

Nearly a decade after the referendum, the broad answer is now clearer. Brexit has made the UK economy smaller than it otherwise would have been. The effect has not been a sudden collapse, but a gradual and cumulative drag on trade, investment and productivity.

The Trade and Cooperation Agreement avoided tariffs on most goods trade. But it did not preserve anything close to the economic relationship the UK had as a member of the single market and customs union. Firms now face customs checks, rules of origin requirements, regulatory paperwork and the loss of automatic mutual recognition. Services firms, especially in regulated sectors, lost important market access rights. Free movement ended.

These changes increased the cost of doing business with the UK’s largest trading partner. Standard trade theory predicted reductions in trade, investment and, over time, productivity.

The evidence now points strongly in that direction. Early estimates, produced soon after the referendum, were necessarily tentative. They had little post-Brexit data to work with and had to separate the effects of Brexit from Covid 19, the energy shock and wider global disruption. But as more data have accumulated, a clearer picture has emerged.

Most serious estimates now suggest that UK GDP is several percentage points below where it would otherwise have been. The Office for Budget Responsibility has long assumed that Brexit will reduce long-run productivity by around 4%, largely because lower trade intensity makes the economy less open and less productive. Other studies, using synthetic control methods or firm-level evidence, produce estimates in the same broad range, and sometimes larger.

The precise number matters less than the direction and persistence of the effect. Brexit did not cause an immediate recession after 2016. Nor did trade with Europe simply stop. But that was never the most plausible mechanism. The more important effect is cumulative: fewer firms trading, weaker investment, lower competitive pressure, less integration into European supply chains, and a reduced flow of knowledge and technology across borders.

Trade is the most direct channel. The UK’s goods trade has underperformed relative to both pre-Brexit trends and comparable economies. Estimates commonly suggest that goods exports are around 10–15% lower than they would otherwise have been, with similar effects on imports.

One apparent puzzle is that the aggregate data do not always show a simple collapse in UK-EU trade relative to trade with the rest of the world. But this is less reassuring than it looks. Brexit has affected the UK’s position in global value chains, not just bilateral trade with the EU. If a UK firm becomes less attractive as part of a European supply chain, it may lose business with both EU and non-EU partners.

There is also a firm-size effect. Large firms are better able to absorb new administrative and regulatory costs. Smaller firms are less able to do so. The result is that aggregate trade flows can look relatively resilient while the number of firms exporting to the EU falls. That matters, because exporting is one route through which smaller firms grow, innovate and become more productive.

Services trade is more mixed. The UK has strengths in high-value, digitally deliverable services, and these have proved more resilient than goods. But this aggregate resilience conceals sectoral losses. Financial services, legal services and other regulated sectors have faced new barriers because the TCA provides only limited access compared with single market membership.

Investment may be the most economically significant channel. Brexit produced a clear rise in uncertainty and a reduction in expected returns for firms using the UK as a base for European markets.

This matters because productivity growth depends heavily on investment. If investment is lower for a sustained period, the economy’s productive capacity suffers. Brexit has therefore compounded one of the UK’s pre-existing weaknesses: poor productivity performance since the financial crisis.

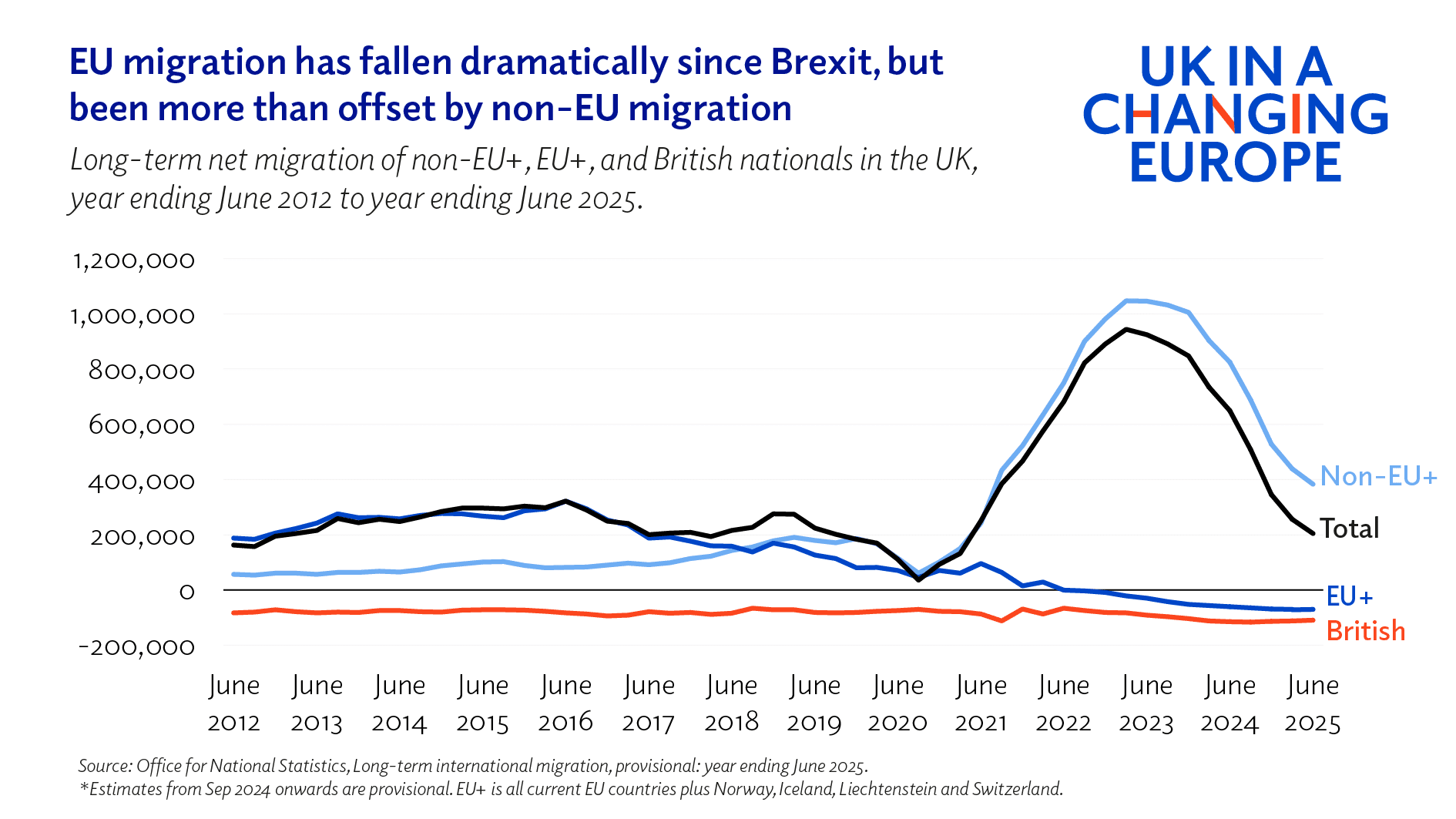

The migration story is different. The end of free movement did reduce EU migration sharply. Sectors such as hospitality, agriculture, logistics, food processing and parts of manufacturing lost access to a familiar and flexible labour supply. In many cases, adjustment came not through large wage rises, but through higher prices, reduced output or changes in business models.

But the post-Brexit immigration system has also allowed much higher non-EU migration, especially through work and study routes. This has more than offset the fall in EU migration in aggregate terms. The result has been a compositional change rather than a simple reduction in migration.

Economically, this is more ambiguous than the trade story. Overall, migration changes have probably raised total GDP relative to a scenario with lower migration, but their effect on GDP per head is smaller and harder to pin down.

The broader problem is that Brexit has made the UK’s existing economic challenges harder to solve. The country already had weak productivity growth, low investment, strained public finances and large regional inequalities. Reducing trade intensity and weakening investment worsen those problems. A smaller economy also means lower tax revenues, which limits the fiscal room for governments to improve public services or reduce taxes.

What about the gains from autonomy? In principle, the UK can now regulate differently, set its own trade policy and design its own migration system. In practice, the economic benefits have so far been limited. Regulatory divergence can create opportunities in specific areas, but it also increases costs in many others. New trade agreements with non-EU countries may bring some benefits, but official estimates suggest these are small compared with the costs of reduced EU integration.

The May 2025 UK-EU ‘Common Understanding’ should be seen in this context. Agreements that reduce checks on agri-food trade, improve professional mobility, ease regulatory frictions or support cooperation in specific sectors would reduce costs for some firms. Smaller exporters, in particular, could benefit from lower fixed costs. But such measures cannot replicate the economic value of single market membership.

Brexit has therefore not produced an economic crisis in the conventional sense. The UK economy has continued to grow, unemployment remains relatively low, and many firms have adapted. But adaptation is not the same as absence of cost. The more relevant counterfactual is not whether the economy is still functioning, but how much better it might have performed; on that question, the evidence is increasingly settled.

By Professor Jonathan Portes, Professor of Economics and Public Policy, Department of Political Economy, King’s College London.